Power Transit: The New U.S.–India–Gulf Triangle

The U.S.–India–Gulf corridor was billed as a new trade spine linking Asia, the Middle East, and Europe. Two years later, war, rivalry, and shifting alliances have exposed its limits, and revealed how connectivity itself has become a front in global power politics.

At first glance, it looked like another conference photo op: flags, handshakes, and a suitably beige backdrop somewhere in Abu Dhabi. Yet the quiet revival of the U.S.–India–Gulf coordination, anchored by transport, energy, and digital infrastructure, may prove one of the decade’s more durable strategic pivots.

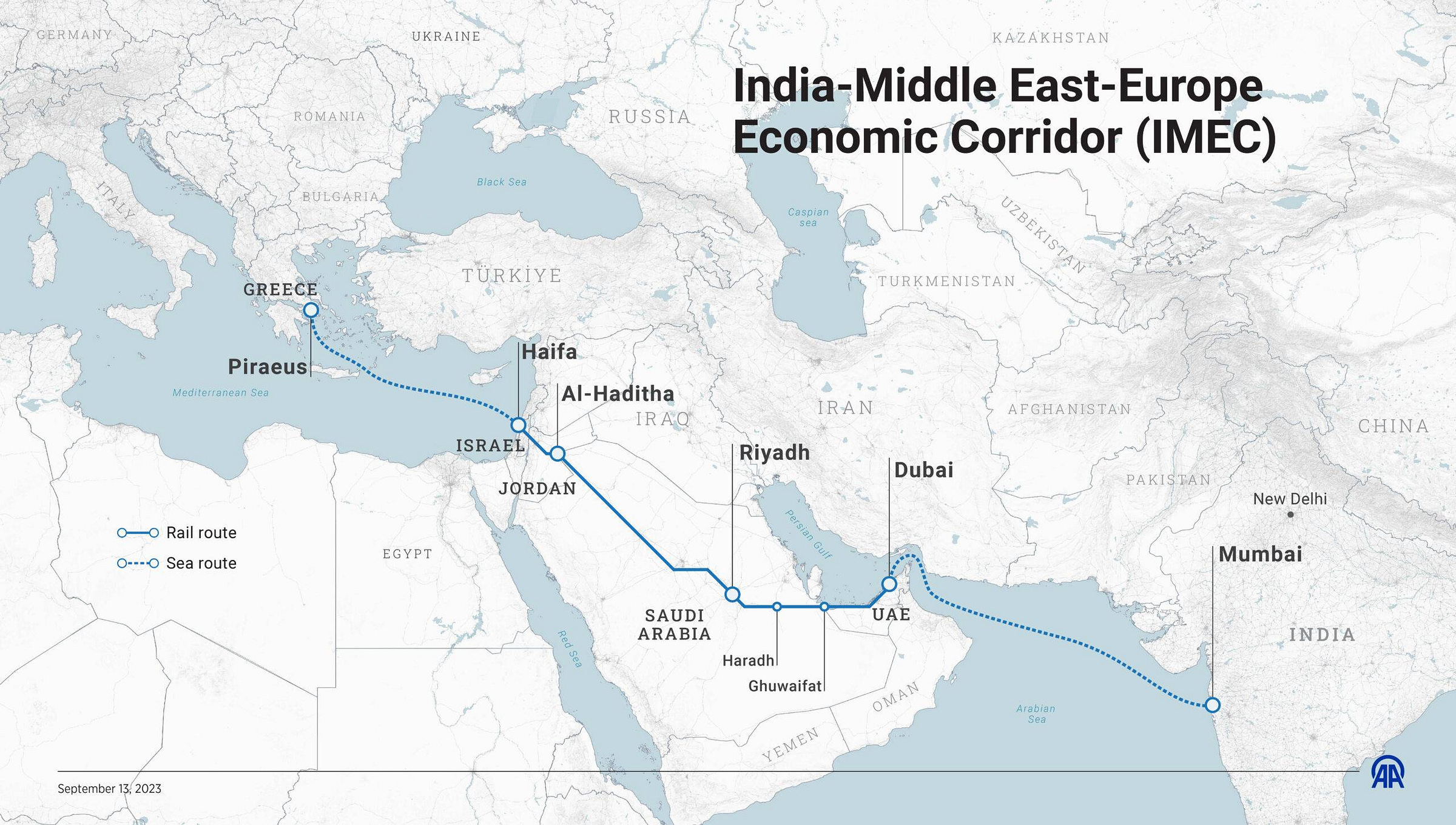

The idea gained public shape at the G20 summit in New Delhi in 2023, when Washington, New Delhi, Riyadh, and Brussels announced the India–Middle East–Europe Economic Corridor (IMEC), a planned network of rail, port, and data-link projects to rival China’s Belt and Road Initiative (Al Jazeera). While headlines quickly faded, follow-up meetings in 2024 and 2025 signaled a certain persistence to the project. Perhaps, it seemed, behind the acronyms, a new triangle of convenience is actually taking shape.

From summit slogans to steel

In 2025, the U.S. quietly approved initial financing through its Development Finance Corporation (DFC) and EXIM Bank to support Gulf-Indian port linkages (DFC). India’s Adani Ports and Saudi Arabia’s PIF-backed logistics ventures have begun scoping out terminals in Gujarat and Jeddah, while the UAE-based DP World has signed memoranda to manage logistics nodes feeding freight toward Haifa, purchased by an Indian consortium in 2023 (Economic Times).

This is a story told not through carriers, frigates, and naval power projections, rather, through cranes and fiber. The corridor’s logic is geo-economic: moving energy, goods, and data faster across trusted routes, cutting traditional exposure to chokepoints like Suez and the Red Sea. For Washington, this supplies a counterweight to China’s Belt and Road-powered westward rail corridors; for India, it opens alternative energy and export paths; and for Gulf monarchies, it hedges between superpowers while monetizing the connectivity in the ‘middle ground’.

India’s dual choreography

New Delhi remains the fulcrum in the mix, the swing actor. Prime Minister Modi’s government has leveraged its G20 host year into sustained infrastructure diplomacy, joining both Western and Gulf financing without formally joining any bloc. The choreography required, however, has been delicate.

India still imports more crude from Russia and the Gulf than ever, while managing a sensitive border freeze with China. The same month Indian ministers met U.S. counterparts in Washington to expand semiconductor cooperation, they hosted Chinese officials at the Shanghai Cooperation Organization (SCO) summit in Tianjin. The result is an unmistakable ‘poly-alignment’: India inserts itself into every corridor, U.S.-led, Gulf-financed, or China-built, but signs no exclusive vows to either. The aim is to develop a deliberate balance between all parties and interests. (Brookings).

Gulf pragmatism, rebranded

For Saudi Arabia and the UAE, the triangle fits their overall strategy of post-oil diversification, as both see logistics, digital infrastructure, and green tech as bridges to a less carbon-intensive economy. Riyadh’s Vision 2030 logistics cluster aims to triple port throughput, while Abu Dhabi’s ADQ and Mubadala funds are quietly bankrolling renewable-heavy industrial zones tied to Indian supply chains (Arab News).

Perhaps more importantly, trade may be setting the stage for a certain thaw in overall tensions. After a decade of tense rivalry, the region’s diplomacy has followed suit, with Riyadh and Tehran re-establishing relations in 2023 via Chinese mediation, and both Saudi Arabia and the UAE formally joined BRICS in 2024. Yet, neither has abandoned security ties with Washington. Instead, they are arbitraging great-power competition, ‘middle-manning’ in a manner not too dissimilar to that of India: selling oil to China, buying arms from the U.S., and attracting Indian engineers and project managers into Gulf industrial zones.

Yet the viability of the entire corridor risks disruption: Israel’s war in Gaza is already complicating plans for the India–Middle East–Europe corridor, injecting the element of uncertainty into logistics, chilling investment appetite, and making the Haifa route more politically fraught (Geopolitical Monitor).

The Gulf’s diversification drive is also reshaping the geography of influence. Saudi Arabia’s Vision 2030 projects and the UAE’s manufacturing corridors are drawing in Indian capital and technical expertise, while nearby Oman’s Duqm port, developed largely with Chinese financing, illustrates how the same maritime arc is contested by multiple partners. Duqm shows how the U.S.–India–Gulf corridor sits inside a wider competition for influence across the western Indian Ocean (The Diplomat).

China: the corridor’s invisible competitor

Beijing reads IMEC as ‘containment by infrastructure’, its planners having spent fifteen years embedding Belt and Road projects across the same geography, from Pakistan’s Gwadar to Egypt’s Port Said. However, momentum has been slowed by capacity strains, debt fatigue, and a liberal dash of regional skepticism, while the IMEC announcement was interpreted in Beijing as an explicit challenge (MERICS).

Still, China’s economic presence remains unmatched: its firms, as proxies for Beijing’s planning, build the cables, turbines, and batteries that underpin much of the Gulf’s diversification drive. The difference, however, lies in the narrative: where China sells connectivity as solidarity, the U.S.–India–Gulf axis seeks to sell it as resilience.

The energy dimension

Energy remains both a catalyst and a constraint. Gulf exporters need a predictable funnel of Asian demand; India needs affordable supply; and the U.S. wants, on the surface at least, decarbonization without price shocks. This triangular logic converges around clean energy corridors: green hydrogen hubs in Oman, ammonia pipelines to India, and joint R&D under the India–U.S. Strategic Clean Energy Partnership (U.S. State Department).

Yet the practiced reality is somewhat off the advertised mark, and transition timelines differ. Gulf producers still expand fossil output even while touting hydrogen; India’s coal dependence persists quite defiantly; and Washington’s politics swing with each election, the current administration’s attitude to anything ‘green’ being a major sticking point to legitimizing transition projects. The risk, therefore, is a corridor defined by contradictory velocities: fast trade, slow transition.

Politics of payment

The financial wiring tells another story. Settling trade in local currencies is the fashionable cause of the Global South, yet in practice, the dollar still dominates. The UAE and India trialed rupee-dirham settlements in 2024, but volumes remain small (Business Standard), and U.S. banks continue to clear most cross-border energy transactions, something that gives Washington leverage, even without troops or tariffs.

If anything, the new triangle moves the impetus away from local currencies and reinforces dollar resilience: Gulf sovereign funds invest in U.S. treasuries, Indian firms borrow in New York, and project financing flows through Western insurance pools.

A corridor, not a bloc

For all its geopolitical geometry, the triangle is not in any sense a security pact, lacking binding guarantees and formal institutions. What holds it together is momentum: a shared belief that infrastructure can substitute for ideology. That belief will be tested by regional volatility, from Yemen’s shipping disruptions to the fragile detente between Israel and the Gulf states.

In practice, the initiative’s success will depend less on memoranda than on whether physical development actually ensues, if we see cranes rise in ports like Duqm, Haifa, and Mundra. If they do, the IMEC could mature into something more substantial and enduring, a genuine connective spine between Asia, the Gulf, and Europe. If they don’t, it will join the long list of unrecognized acronyms.

Why it matters

For readers tracking the evolution of global order, the U.S.–India–Gulf triangle is a microcosm of the current age: transactional, multi-polar, and led by infrastructure. It illustrates how states now project influence through grids, cables, and ports, rather than pacts or bases. It’s something we’re consistently seeing at GYST, and will continue to note in this era of fracturing and shifting alignments.

The triangle’s durability, however, will rest on whether its members can align timelines: Washington’s divisive political cycles, India’s sometimes indiscernible development pace, and the Gulf’s often opaque decarbonization sprint. The choreography is intricate but, nevertheless, consequential. The direction of twenty-first-century power may be traced not along frontlines, but along freight lines.

Read this. Notice that. Do something.

Read this: Al Jazeera on IMEC’s unveiling at the 2023 G20 summit; MERICS on Beijing’s direction; U.S. State Department joint statement on the India–U.S. Clean Energy Partnership.

Notice that: the triangle is commercial, not military; the U.S. regains leverage via finance, not force; and India’s balancing act grows harder as both Beijing and Washington court the Gulf.

Do something: follow where the ports rise and the pipes run, these routes will map the next geopolitical order.

Previously on GYST: BRICS and the illusion of unity

Next up: The Silent Harvest: China’s Soybean Split